Polyurethanes

Overview

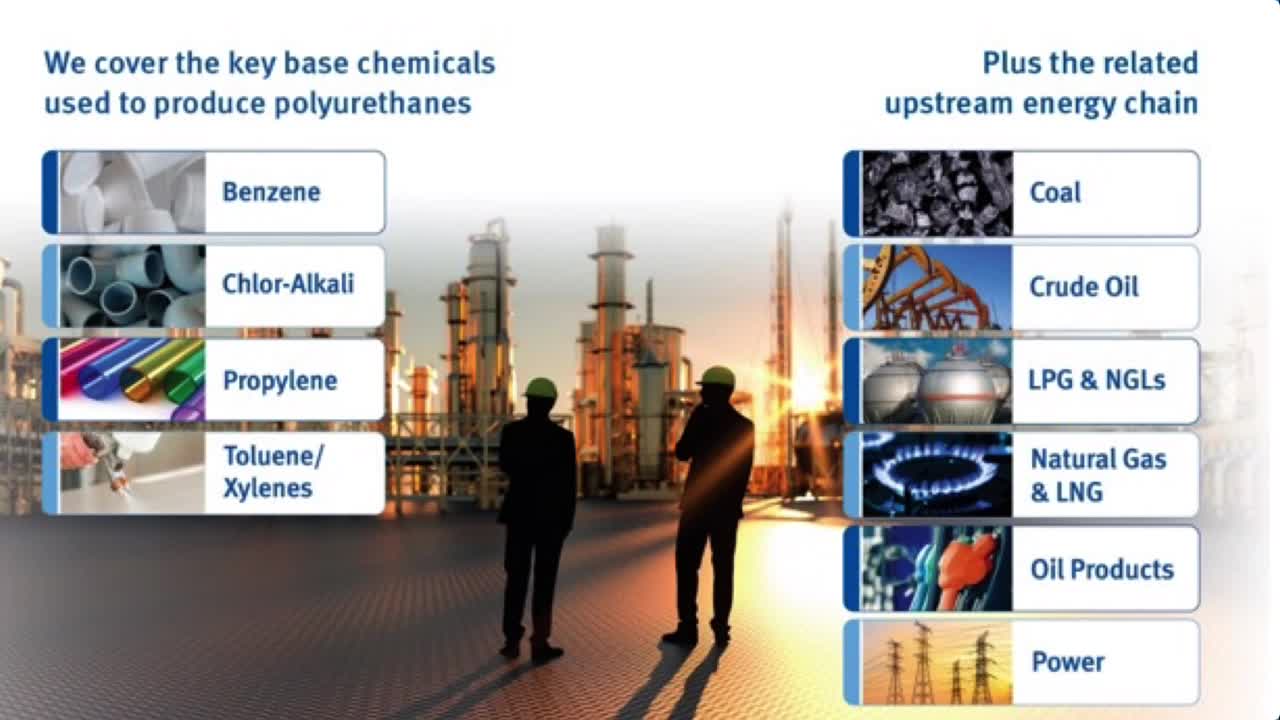

Polyurethanes are a feature of everyday life. They’re present in our furniture, bedding, clothes, shoes, buildings, and cars. The journey from base chemicals such as propylene or benzene to end-use polyurethanes involves multiple steps and chemical products. Argus can help you to navigate this complex and volatile value chain and make better commercial decisions around sales, marketing, distribution and procurement.

Argus’ polyurethanes services give you in-depth global and regional pricing insight, including feedstock analysis, in single, concise and integrated reports. In addition to pricing, you get access to global industry news and analysis of key economic drivers on a weekly basis. We cover isocyanates, propylene oxide, propylene glycols and polyols.

Video: Argus polyurethanes services

Latest polyurethanes news

Browse the latest market moving news on the global polyurethanes industry.

Falling mortgage rates may boost US housing, PVC

Falling mortgage rates may boost US housing, PVC

Houston, 6 March (Argus) — US mortgage rates this year have sunk to their lowest level in more than three years and could unlock more consumer demand in a housing sector that has faced falling affordability . But tepid early-year housing demand has left polyvinyl chloride (PVC) suppliers cautiously optimistic that demand in the housing market could strengthen compared with 2025, with most expectations centered around a repeat of last year. About 51pc of outstanding mortgages have interest rates below 4pc, according to third quarter 2025 data from the US Federal Housing Finance Agency. With current rates as much as 50pc higher, that means more current homeowners who would otherwise be in the market for a new home are staying put. Realtors and mortgage experts anticipate a nominal rebound in housing demand this year as average rates on a 30-year mortgage slumped below 6pc for the week ended 27 February — the first time in more than three years — before crawling back to an average 6pc this week, Freddie Mac data show. "Rates below 6pc are an important psychological milestone for both buyers and sellers," said Nadia Evangelou, senior economist and director of real estate research at the National Association of Realtors (NAR). "Nearly 5.5mn additional households can afford the median-priced home when rates fall from 7pc to 6pc." Housing affordability improved early this year on higher income and declining interest rates. Gradually higher purchasing power early this year underpins expectations of an 8pc increase in 2026 home sales and indicates an anemic US housing sector could be at an inflection point, data from the Mortgage Bankers Association (MBA) show. But new-home construction remains subdued, and a marginal decrease from 2025 is still expected. The MBA forecasts a 2pc decline this year in total housing starts from 2025, while the NAR projects a 1pc increase in single-family starts. Bullish demand signals in the domestic housing market have not shifted outlooks from PVC suppliers, who are maintaining tempered demand expectations from home construction. Current outlooks largely anticipate PVC demand into new-home construction to mirror 2025, which extended the multi-year demand slump in the sector. Instead, PVC suppliers are increasingly bullish on rebounding demand in the remodeling and wiring and cable industries, sources said. Residential remodeling activity is expected to grow by 3pc in 2026 and by 2pc in 2027, data from the National Association of Home Builders show. This trend is supported by an aging housing stock, homeowners locked into lower mortgage rates, and older homeowners not purchasing new homes. US home builders share the PVC industry's cautious outlook. A survey of home builders in February continued to paint a cooling new-home market, data from the NAHB/Wells Fargo Housing Market Index show. The leading concerns for surveyed builders are buyers waiting for lower mortgage rates, concerns about the broader economic environment, and high Federal Reserve interest rates. The US Federal Reserve is generally not expected to reduce its target interest rate in the first half of the year, with expectations of rate cuts in 2026 significantly dampened by stubbornly-high inflation and weaker-than-expected employment numbers in recent months, CME FedWatch data show. By Maya Porter and Gordon Pollock Mortgage rates vs. Residential construction permits Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

EU conditionally clears Adnoc-Covestro deal under FSR

EU conditionally clears Adnoc-Covestro deal under FSR

London, 14 November (Argus) — The European Commission has given conditional approval to plans by Abu Dhabi's state-owned Adnoc to acquire German chemicals group Covestro under the EU's foreign subsidies regulation (FSR). Adnoc, to address the commission's competition concerns relating to state subsidies, offered to adapt its articles of association to make sure they align with UAE insolvency law, thereby removing unlimited guarantee from the state. It will also share Covestro's sustainability patents with certain market participants. "Clear, predefined access to these patents will enable others to innovate and advance research in an area that is critical for Europe's future," commission executive vice president Teresa Ribera said. The commission said these commitments "will balance out the negative effects" of the €12bn ($13.9bn) Adnoc-Covestro deal in the EU market. During an in-depth investigation, the commission found that "Adnoc and Covestro received foreign subsidies from the UAE that are liable to distort the EU internal market." These subsidies include an unlimited state guarantee to Adnoc, as well as a committed capital increase from Adnoc into Covestro. "As a result, the merged entity could have engaged in more aggressive investment strategies than absent the subsidies, to the detriment of other market participants and competitive conditions in the internal market," the commission said. The commission gave the green light to the acquisition in May, but decided to launch an in-depth probe in July under the FSR because of competition concerns relating to state subsidies. The FSR began in July 2023 and allows the commission to address distortion caused by foreign subsidies as a way of ensuring a laying playing field for all companies in the EU market. By Monicca Egoy Send comments and request more information at feedback@argusmedia.com Copyright © 2025. Argus Media group . All rights reserved.

Whirlpool sees 2025 appliance market flat to down

Whirlpool sees 2025 appliance market flat to down

Houston, 28 October (Argus) — Appliance maker Whirlpool anticipates the appliance market to be flat to down slightly, by three percentage points, both overall and for North America this year, Whirlpool said in its third quarter earnings release. Whirlpool's third quarter net sales rose by 1pc to $4bn up from $3.9bn in the prior year because of new product releases, specifically in North America. Whirlpool plans to launch over 100 new products globally in 2025. North American net sales rose by 3pc year over year in the third quarter, strengthened by new product sales. Net sales in Latin America and Asia were down 6pc and 7pc, respectively, because of volume declines. Whirlpool's small domestic appliances (SDA) segment sales increased 10pc in the third quarter supported by new product launches. Of Whirlpool's major appliance products sold in the US, 80pc are produced in the US, lessening the strain poised by tariffs. The company is still battling imports that were front loaded prior to tariffs but is starting to see import inventories and arrivals decline. Appliance makers us polyurethanes for insulation and sealants. Polyurethane demand has been below historic levels this year as tariffs and economic uncertainty have slowed consumer demand, according to market participants. Many polyurethane participants expect next year to look similar to 2025 for appliance application demand. Whirlpool expects recovery in the housing market to benefit the appliance maker as they have a high home builder relationship allowing Whirlpool appliances to be placed in new builds. The US has a shortfall of three to four million housing units, the company said. The company delayed its expectation of the US housing market recovery in 2025 moving it into 2026 to begin a multi-year rebound once interest rates ease. Despite a challenging 2025, the company views its North America business well placed for future growth. Whirlpool reported a $73mn profit in the third quarter, a decrease from $109mn recognized last year. By Catherine Rabe Send comments and request more information at feedback@argusmedia.com Copyright © 2025. Argus Media group . All rights reserved.

Dow to shut Belgian polyols plant by March 2026

Dow to shut Belgian polyols plant by March 2026

London, 2 October (Argus) — US chemical firm Dow will shut its 94,000 t/yr polyether polyols production site at Tertre, Belgium, by the end of March next year, it confirmed to Argus today. The move is part of a broader review of the company's European assets aimed at addressing "the structural challenges of high costs, driven by high energy costs and a burdensome regulatory environment", Dow said. The site is likely to be dismantled after closure, workers' union FGTB said. The plant has three production lines, but two were already idled as part of a restructuring that began in 2023, according to the union. The closure will affect 37 roles and eight contractor positions. Dow said it does not expect any impact to customers and will continue delivering the same product mix. The firm has 530,000 t/yr of polyether polyols capacity at its Terneuzen site in the Netherlands and a further 60,000 t/yr in Tarragona, Spain. Europe's polyether polyols market has been pressured by weak demand and excess production capacity, compounded by rising imports, mainly from Asia. Dow said a loss of competitiveness in the face of increased imports was a key factor in the decision to close the Tertre site. Imports of all polyethers, including polyether polyols, into the EU averaged 286,000 t/yr in 2020–24, with record deliveries of 323,000t last year. Imports in January–July this year were 6.3pc higher than the same period a year earlier. China is the leading supplier, followed by South Korea and Saudi Arabia. Demand from key polyether polyol sectors — including automotive, appliances and soft furnishings — has been hit by limited consumer confidence and lower spending on durable goods. Demand from the construction sector has also faltered on economic uncertainty and a weak investment environment. Argus assessed the September contract price for flexible slabstock polyether polyols at €1,030–1,100/t, down from a midpoint of €1,225/t in January and 24pc lower than the September 2024 price. Early indications for October suggest continued softening in the polyols market. By Laura Tovey-Fall Send comments and request more information at feedback@argusmedia.com Copyright © 2025. Argus Media group . All rights reserved.

Spotlight content

Browse the latest thought leadership produced by our global team of experts.

PMDI Trade Flow Map 2024

US MDI trade, tariffs and market balance infographic

US President Donald Trump has stated new and additional tariffs could be introduced on imports from various trading partners.